Sustainia Simplifies

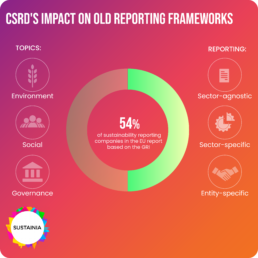

CSRD's Impact on Old Reporting Frameworks in EU

With its sights set on achieving a carbon-neutral Europe by 2050, the European Union (EU) has introduced the Corporate Sustainability Reporting Directive (CSRD) to continue its efforts towards sustainable use and maintenance of resources.

The future is uncertain for some

The regulation will affect approximately 50.000 companies – including large companies in the EU, companies listed on EU-regulated markets, and non-EU companies with branches or subsidiaries in the EU – and mandates said companies to document and report a wide range of sustainability issues based on the guidelines set out under the European Sustainability Reporting Standards (ESRS) starting from 2024.

Before the conception of the CSRD, sustainability reporting was not an unknown concept, as many European companies already adhered to at least one reporting framework, including the Non-Financial Reporting Directive (NFRD), The Global Reporting Initiative (GRI), and the Task Force on Climate-Related Financial Disclosures (TCFD).

While the NFRD, which currently applies to around 11.700 companies within the European Union, will be replaced by the CSRD, the futures of the GRI and TCFD are uncertain given that they are non-mandatory reporting frameworks. Considering around 54% of sustainability-reporting companies in the EU currently report based on the GRI and a considerable number are well aligned with the TCFD recommendations, it is crucial to consider their long-term use, value, and validity, especially regarding sustainability reporting in the region.

With CSRD, the Annual Report is King

Besides the obvious mandatory/non-mandatory distinction, the CSRD is unequivocal about mandatory disclosures to be included in companies’ annual reports. Guided by the “Environmental Social & Governance (ESG)” tenets, corporations must provide relevant information on sustainability issues that are material to their operations, risks, and strategies. These disclosures aim to provide investors and stakeholders with more comprehensive information about companies’ sustainability practices, risks, and opportunities.

By contrast, the GRI and TCFD provide guidance on what to disclose but do not require specific disclosures. Essentially, this affords flexibility in choosing sustainability topics to report on and how to present the information. The “annual report requirement” will not only ensure that all material ESG issues are reported but also mandates their inclusion in corporations’ annual reports. This eliminates the need for standalone sustainability reports enabled by the GRI framework.

Another significant advantage of the CSRD is that it enhances the transparency and comparability of sustainability risks, opportunities, impact, and reporting among affected companies in the European Union. For example, the CSRD successfully integrates GRI and TCFD recommendations, such as “double materiality” and report audits, to aid the transition.

Conversely, CSRD implementation poses significant challenges such as compliance costs, especially for smaller companies that lack resources or expertise, increased burden, particularly regarding information gathering and accuracy in complex supply chains, and standardisation challenges due to varied CSRD and ESRS interpretations.

The success of CSRD relies on GRI and TCFD

While the GRI and TCFD frameworks remain structurally pristine outside the EU and among EU companies not currently affected by the CSRD, the emergence of the CSRD in the region all but eliminates the need for sustainability reporting based on the familiar frameworks. Considering the extensive reporting requirements of the CSRD, coupled with the time, costs, and resources involved, it is onerous to contemplate a scenario where companies previously subscribed to the GRI, and TCFD retain those erstwhile structures.

Alternatively, if time, costs, and resources were not an issue for certain entities, attempts to maintain GRI and TCFD frameworks in standalone sustainability reports could complement the CSRD, since the latter only requires that material disclosures be included in companies’ annual reports.

However, this would likely draw attention away from annual reports, thus defeating the transparency and comparability criteria. It is easier to envision a future where the GRI structure and TCFD recommendations are vital in improving the CSRD. The CSRD is new but not novel. With the GRI’s involvement in providing technical input to the development of the ESRS and the EU’s continued dependence on the TCFD recommendations, the CSRD’s foundation is deeply rooted in GRI and TCFD structures.

The CSRD is a significant step forward in sustainability reporting for EU companies, mandating comprehensive reporting on material ESG issues. While the futures of non-mandatory reporting frameworks such as GRI and TCFD appear gloomy, the CSRD’s integration of their recommendations provides a solid foundation for future improvements. Compliance costs, information-gathering burdens, and standardisation challenges exist, but the CSRD’s transparency and comparability benefits outweigh these challenges.